فريقنا لديه أكثر من 7,000,000 من التجار!

كل يوم نعمل معا لتحسين التداول. نحصل على نتائج عالية ونمضي قدما.

الاعتراف من قبل الملايين من التجار في جميع أنحاء العالم هو أفضل تقدير لعملنا! لقد قمت باختيارك وسنفعل كل ما يلزم لتلبية توقعاتك!

نحن فريق رائع معا!

إنستافوركس تعتز بالعمل بالنسبة لك!

الممثل وبطل مسابقة يو إف سي 6 وبطل حقيقي!

الرجل الذي حقق النجاح بعمله الدؤوب. الرجل الذي يذهب كما نريد.

سر نجاح تاكتاروف هو حركة مستمرة نحو الهدف.

اكشف عن جميع جوانب موهبتك!

اكتشف، وحاول، وافشل - ولكن لا تتوقف أبدا!

إنستافوركس. تبدأ قصة نجاحك من هنا!

Retail sales in the US in April were above forecasts, the so-called control group sales grew by 0.7% (forecast 0.4%), which led to a rise in inflation expectations and an increase in UST yields. A Pfizer deal for $31 billion, close to the record for all corporate bond transactions, also contributed to higher yields.

The industrial production report was also significantly better than forecasts - capacity utilization reached 79.9%, and production itself grew by 0.5% (zero growth was forecasted). The NAHB housing market index also surprised with a noticeable decline in sales of existing homes.

All indicators, directly or indirectly, point to an increase in inflation expectations, which allowed the Fed's rate forecasts to be adjusted in a more hawkish direction.

All key indicators of activity in China - retail sales, industrial production, and investments - showed worse dynamics than forecasts in April. These reports came later than import and inflation data, which also showed a slowdown. Overall, weaker data from China affect commodity currencies, primarily NZD and AUD, and also increase the risks of a global recession, which could support demand for protective assets.

The negotiations on the US debt ceiling have a strong impact on the markets. House Speaker McCarthy said that an agreement could be expected by the end of the week. But as long as there is no agreement, the markets will most likely take a wait-and-see position and there will be no strong movements.

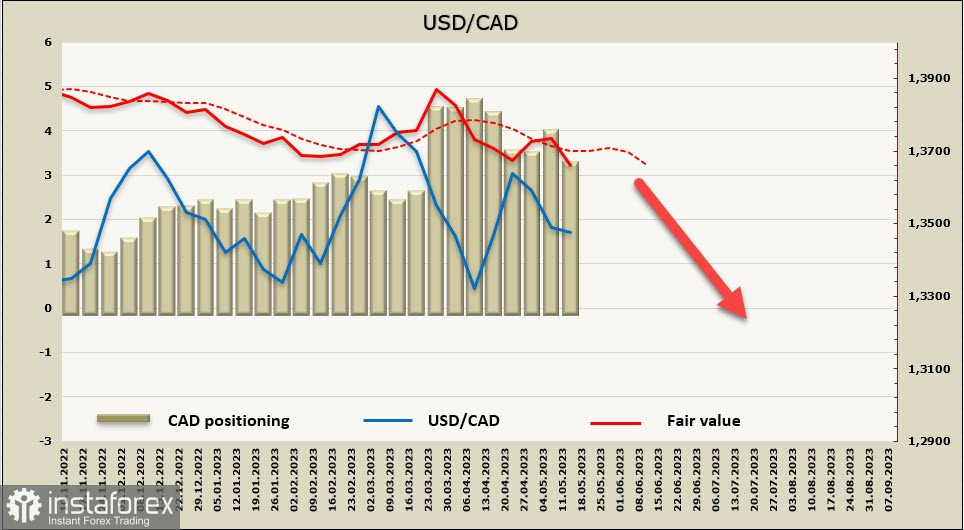

USD/CAD

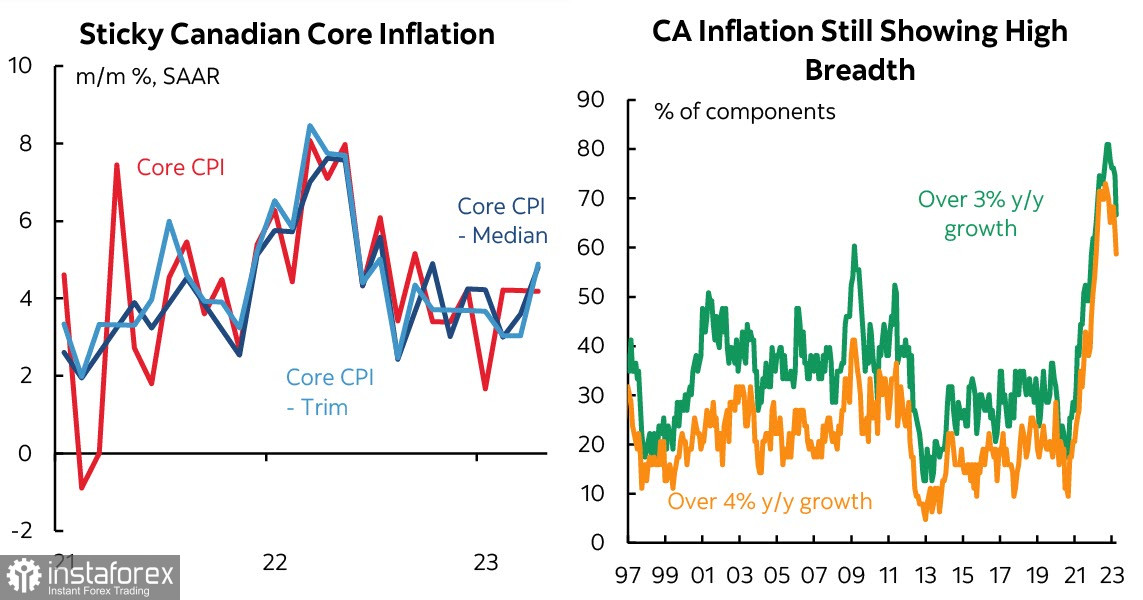

Inflation in Canada did not show signs of slowing down in April. The general index rose from 4.3% y/y to 4.4% (forecast 4.1%), and the Canadian dollar could have strengthened against the USD if not for strong data from the US (on retail sales and industrial production).

All three indicators of core inflation have stopped declining, and a resumption of growth can be seen.

The forecast for the Bank of Canada's rate has increased, and the growth of expectations will be the determining factor in the coming week, which will allow the bulls on CAD to increase their activity.

The net short position on CAD decreased by 0.5 billion over the reporting week, to -3.2 billion. Speculative positioning is still bearish, but there is a trend in favor of buying the Canadian currency, and the settlement price has dropped below the long-term average.

USD/CAD continues to trade in a range that increasingly takes the form of a converging triangle. Resistance is at 1.3560, with the movement towards the lower boundary of the pattern at 1.3330/40 seeming more likely. As of Wednesday morning, a downward break out of the range appears more likely. In case of a downward movement, the next target will be the boundary of the horizontal channel at 1.3224.

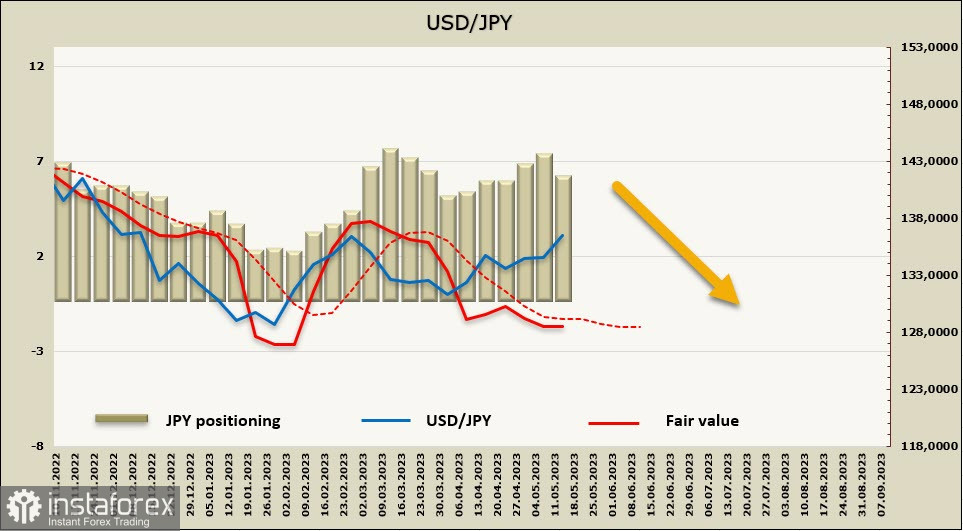

USD/JPY

Japan's Cabinet Office published the first preliminary estimate of GDP for the first quarter, with real GDP increasing by 0.4% q/q (forecast 0.1%), with all growth being ensured exclusively by domestic demand. Consumer spending increased by 0.6%, and capital expenditure by 0.9%.

At the same time, exports of goods and services decreased by 4.2%, and the Cabinet sees no driver for the Japanese economy to pick up the pace of recovery. This is one of the reasons why the abandonment of stimulus policies may be postponed, so the yen continued to be sold after the report's release.

The yen remains the main safe-haven currency, even though continued stimulus policies are at odds with the direction of other central banks. In terms of current operations, Japan maintains a positive balance, the trade balance deficit is not growing, primary income has a significant surplus, in the 22nd fiscal year it exceeded 9 trillion yen and covers both the trade deficit and the secondary income deficit.

Also, it is worth noting the political stability in Japan, as well as the fact that the markets are still waiting for hints of winding down the stimulus program. As soon as this happens, the yen will receive a strong driver for strengthening.

The net short position on JPY decreased by 0.6 billion over the reporting week to -5.6 billion, the bias is bearish, but the settlement price continues to stubbornly stay below the long-term average, which allows adhering to the conclusion about the corrective growth of USD/JPY.

In the previous review, we assumed that the corrective growth of USD/JPY may end after updating the local maximum of 137.92, the pair continues to move towards this goal, where a reversal can be expected. From a technical point of view, short-term trends indicate the continuation of growth, however, it can end at any moment as soon as fundamental factors come into play.

*The market analysis posted here is meant to increase your awareness, but not to give instructions to make a trade.

InstaSpot analytical reviews will make you fully aware of market trends! Being an InstaSpot client, you are provided with a large number of free services for efficient trading.