U.S. indices Nasdaq and S&P 500 closed Thursday on a positive note, thanks to Tesla's promising outlook and a drop in Treasury yields from recent highs. Despite some mixed corporate earnings, Tesla's strong performance helped keep Wall Street's spirits high.

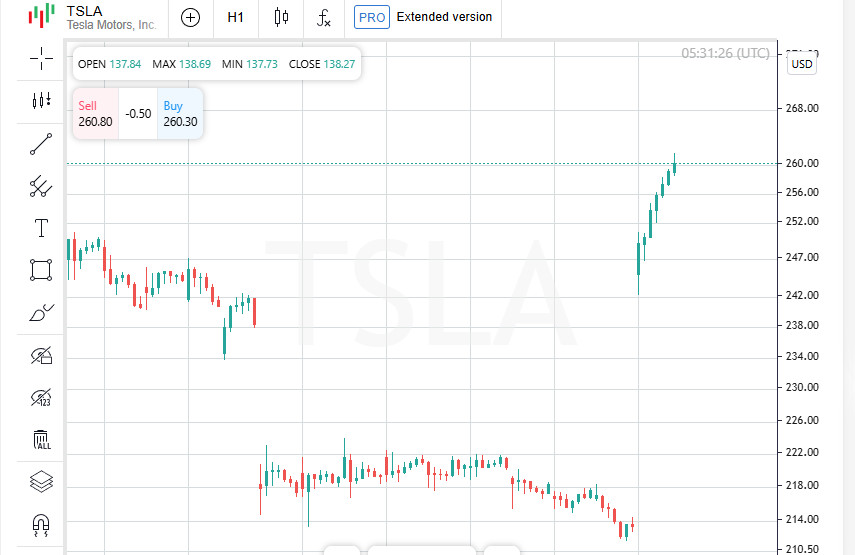

Tesla shares surged by 21.9%, adding over $140 billion to its market cap. The electric vehicle giant's stock jump came after robust third-quarter results and optimistic forecasts for 2024: Tesla projects a 20–30% sales growth, inspiring investors to increase their stakes.

Tesla's growth also boosted related sectors. The consumer discretionary sector (.SPLRCD) rose by 3.24%. "This was a pivotal moment for Tesla," commented Charlie Ripley, senior investment strategist at Allianz Investment Management, highlighting how the company's success fuels momentum across related sectors.

The S&P index ended the day with its first gain of the week, although overall sentiment remained cautious. Most sectors in the S&P finished in the red as, despite the dip in bond yields, they remain high, creating pressure on the market. The 10-year Treasury yield dropped to 4.20%, retreating from 4.26% the previous day when all three major U.S. indices had also lost ground.

While Tesla's performance and lower bond yields supported the market, participants still view future prospects with caution.

According to Bill Northey, senior investment director at U.S. Bank Wealth Management, active rate hikes have influenced market dynamics in October. "The sharp rise in the 10-year Treasury yields, which were below 4% just recently, to the current levels has been exceptionally swift," Northey noted, underscoring the role of the bond market in recent shifts.

Among companies reporting pre-market, IBM and Honeywell both missed expectations. IBM's shares fell by 6.17% following a weak third-quarter revenue report, while Honeywell declined by 5.10% after delivering a disappointing sales forecast. These misses added pressure on the Dow Jones, representing the U.S. market's blue-chip firms.

The stock market closed with mixed results: the Dow Jones Industrial Average (.DJI) lost 140.59 points, or 0.33%, to close at 42,374.36, while the S&P 500 (.SPX) added 12.44 points (+0.21%) to finish at 5,809.86. The Nasdaq Composite (.IXIC) also showed confident growth, gaining 138.83 points (+0.76%) to reach 18,415.49. Support from tech sector stocks helped Nasdaq hold its ground despite mixed results across other sectors.

The materials sector (.SPLRCM) faced pressure, dropping by 1.42%. The main contributor to this decline was Newmont, which missed profit expectations due to rising costs and lower production in Nevada.

Boeing also struggled: its shares fell by 1.18% following news of an ongoing strike at one of the company's plants. Workers voted against a proposed contract, prolonging a strike that has been ongoing for more than five weeks, adding uncertainty to Boeing's future production plans.

U.S. stocks retreated from recent record highs over the last few sessions as investors reassessed their expectations for a Federal Reserve rate cut amid increasing Treasury yields, mixed corporate earnings, and uncertainty around upcoming U.S. elections.

Despite the correction, Triple D Trading's Dennis Dick remains optimistic: "The tech story remains relevant, and that story isn't over. I still believe tech sector pullbacks are buying opportunities," he said, pointing to opportunities for investors.

Southwest Airlines (LUV.N) shares dropped by 5.56% following the company's earnings report and news of a settlement with activist fund Elliott Investment Management. While sentiment in the airline sector remained subdued, UPS (UPS.N) moved in the opposite direction: its shares rose by 5.28% after a third-quarter earnings report showing increased volumes and cost reductions. UPS has been capitalizing on its operational efficiency and rising demand.

According to data from LSEG, of the 159 companies in the S&P 500 that reported quarterly results, 78.6% exceeded analysts' expectations. This shows that, despite tensions around rates and political uncertainty, a significant portion of the U.S. market remains resilient and adaptable.

In October, U.S. business activity continued to expand. Preliminary S&P Global PMI data revealed growth in activity driven by strong demand, alongside a surprise drop in unemployment claims to 227,000 for the week ending October 19. These indicators signal a robust economic foundation that supports the market despite stock volatility.

On the New York Stock Exchange (NYSE), the number of advancing stocks outnumbered decliners in a 1.25-to-1 ratio. Additionally, NYSE recorded 137 new highs and 49 new lows, indicating a positive market sentiment amid recent challenges.

The S&P 500 index marked 41 new 52-week highs and only 3 new lows, while the Nasdaq Composite recorded 76 new highs and 89 new lows. Despite fluctuations, the total trading volume on U.S. exchanges reached 11.06 billion shares, just slightly below the 20-day average of 11.59 billion. This indicates sustained market interest, despite economic and political headwinds.

Global stocks closed Thursday on an upswing, breaking a three-session losing streak amid volatile trading. Positive corporate earnings and a dip in U.S. Treasury yields alleviated investor concerns over upcoming U.S. elections and potential rate cuts.

European markets also managed a slight recovery, climbing 0.03% on positive earnings from Renault, Unilever, and Hermes. Supported by this momentum, the MSCI global index (.MIWD00000PUS) rose 0.2%, reaching 846.07. This suggests cautious optimism among European and global investors closely watching developments on both sides of the Atlantic.

Michael Farr, president and CEO of Farr, Miller & Washington, noted that the last three or four days have served as a kind of breather for global markets after a notable rally. "Despite the recent pullback, most indices are still trading near record highs," he pointed out, adding that the economy remains stable and earnings season is in line with investor expectations.

Commenting on the Fed's upcoming policy, Farr expressed caution, noting that the Fed will likely not cut rates as aggressively or quickly as the market might wish. Nonetheless, he emphasized that the overall economy is performing well, and the corporate earnings season is showing steady growth, which reinforces current market expectations and stability.

According to the latest data from CME Group's FedWatch tool, traders see a nearly 95% chance of a 25 basis-point rate cut by the Federal Reserve at its November meeting. A 3.4 basis-point drop in the 10-year Treasury yield, now at 4.208% following a high of 4.26% the previous day, also reflects these expectations. This rebound in bond prices after July's highs suggests the market is cautiously optimistic about the Fed's upcoming decisions.

Mark Malek, chief investment officer at SiebertNXT, noted that spending promises by U.S. presidential candidates could seriously expand the budget deficit. A growing deficit implies an increase in national debt, which, in turn, places added pressure on bond yields, particularly for 10-year Treasury bonds. Thus, the candidates' plans may have long-term consequences for the debt market, heightening risks for Treasury bonds.

In light of fresh data showing an unexpected drop in jobless claims to 227,000 last week, the U.S. dollar weakened, suggesting a resilient labor market. These labor market insights led investors to anticipate a more gradual pace of rate cuts by the Fed.

The U.S. dollar lost 0.6% against the Japanese yen, hitting 151.84, while the euro gained 0.44% to reach $1.0828. The British pound also rose 0.42% to reach $1.29874. The dollar index, which tracks its value against a basket of key global currencies such as the yen and euro, declined 0.4% to settle at 104.02, signaling softening dollar positions.

A combination of rising budget deficits, increasing national debt, and active fiscal policy discussions surrounding the presidential election continue to shape market sentiment. The debt burden and inflation expectations maintain pressure on the bond market, while currency fluctuations reflect rising uncertainty among investors awaiting the Fed's next moves and the global economic response to U.S. policy.

Gold prices approached near-record highs as investors seek safe-haven assets in response to escalating geopolitical tensions and the upcoming U.S. elections on November 5. Spot gold climbed by 0.69% to $2,736.10 per ounce, while U.S. gold futures rose 0.7% to $2,748.9 per ounce. This surge highlights that gold remains a favored asset, especially in uncertain times.

Oil prices dipped by around 1% during volatile trading as news of potential negotiations between the U.S. and Israel regarding a ceasefire in Gaza added uncertainty to the energy market. Brent crude futures fell by 0.8%, reaching $74.38 per barrel, while West Texas Intermediate (WTI) dropped by 0.8% to $70.19 per barrel. Political developments in the region remain a key factor for oil prices.

"Political events and geopolitical risks, including elections, typically increase short-term market volatility," said Michael Farr, president of Farr, Miller & Washington, "but their impact on stock prices over longer periods tends to be limited." Farr emphasized that despite the recent turbulence, the market remains resilient, and volatility caused by short-term events does not always significantly impact investors' strategic positions.

InstaSpot analytical reviews will make you fully aware of market trends! Being an InstaSpot client, you are provided with a large number of free services for efficient trading.