¡Nuestro equipo cuenta con más de 7,000,000 operadores!

Cada día, trabajamos juntos para mejorar las operaciones. Obtenemos grandes resultados y seguimos adelante.

El reconocimiento de millones de operadores en todo el mundo es el mejor agradecimiento a nuestro trabajo! ¡Usted hizo su elección y haremos todo lo que esté a nuestro alcance para satisfacer sus expectativas!

¡Juntos somos un gran equipo!

InstaSpot. ¡Orgulloso de trabajar para usted!

¡Actor, 6 veces ganador del torneo UFC y un verdadero héroe!

El hombre que se hizo a sí mismo. El hombre que sigue nuestro camino.

El secreto detrás del éxito de Taktarov es el constante movimiento hacia el objetivo.

¡Revele todo los lados de su talento!

Descubra, intente, fracase, ¡pero nunca se rinda!

InstaSpot. ¡Su historia de éxito comienza aquí!

There is no such thing as a free lunch. What were the EUR/USD bulls counting on? That the eurozone economy would grow rapidly and that recent weak business activity data were temporary setbacks? That Donald Trump would stop tweeting and not mentioning Europe in his tariff announcement was good news for the euro? That the European Central Bank would reconsider rate cuts? Unfortunately, all of this is wishful thinking. As such, it's time for the major currency pair to return to its downward trend.

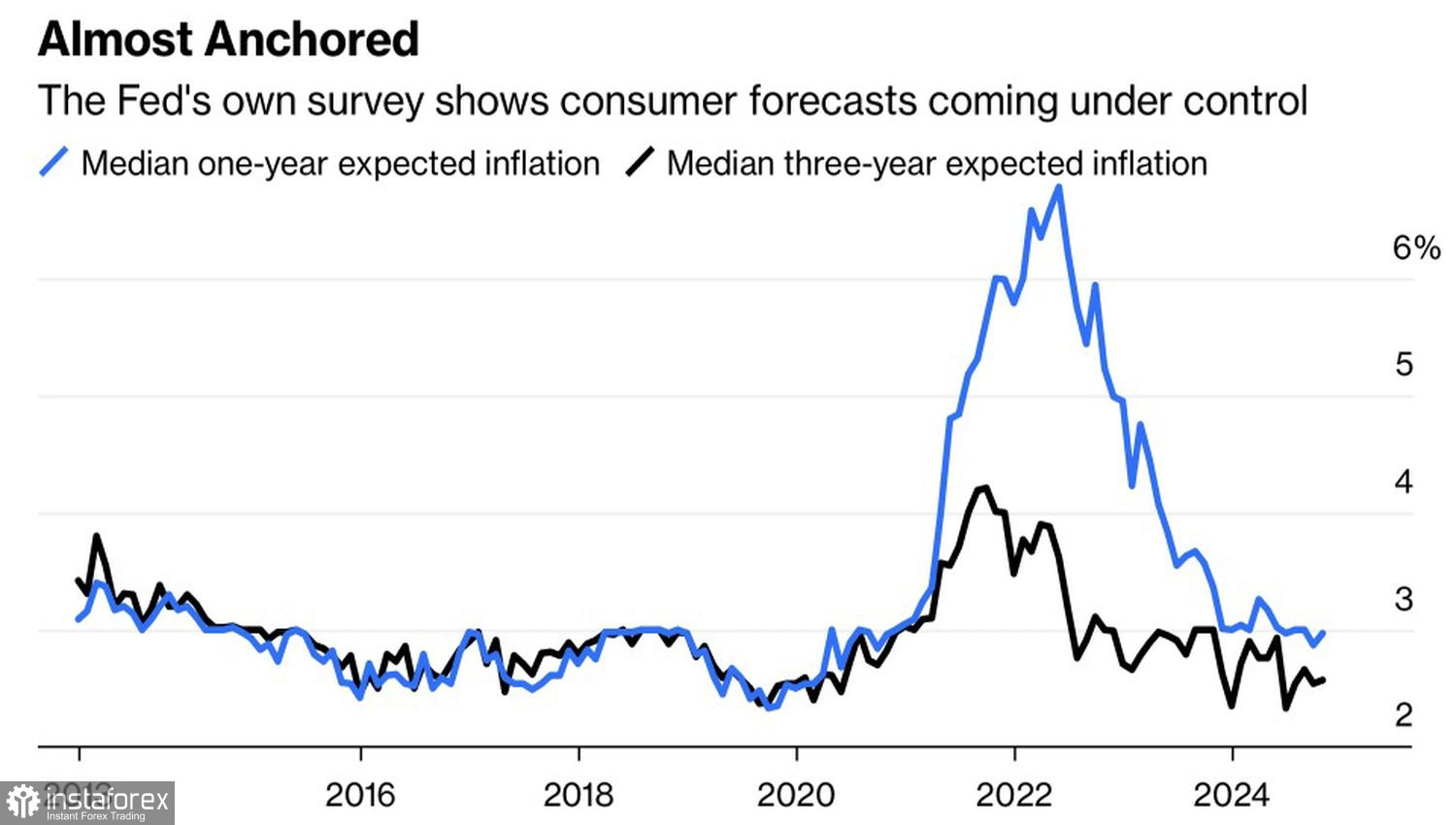

Despite strong data on the U.S. labor market and expectations of faster consumer prices in November, derivatives show an 86% probability of a federal funds rate cut at the December FOMC meeting. The reason? Likely because of the Federal Reserve's inflation expectations, which continue to decline steadily.

Take my word for it – Donald Trump will "fix" everything. His policies of fiscal stimulus and trade tariffs are inflating prices in much the same way the pandemic and its associated supply chain disruptions did. I fear a repeat of the 1970s, when the Fed prematurely declared victory over high prices only to see inflation accelerate, forcing it to resume rate hikes. If this scenario unfolds, the strength of the U.S. dollar will be here to stay.

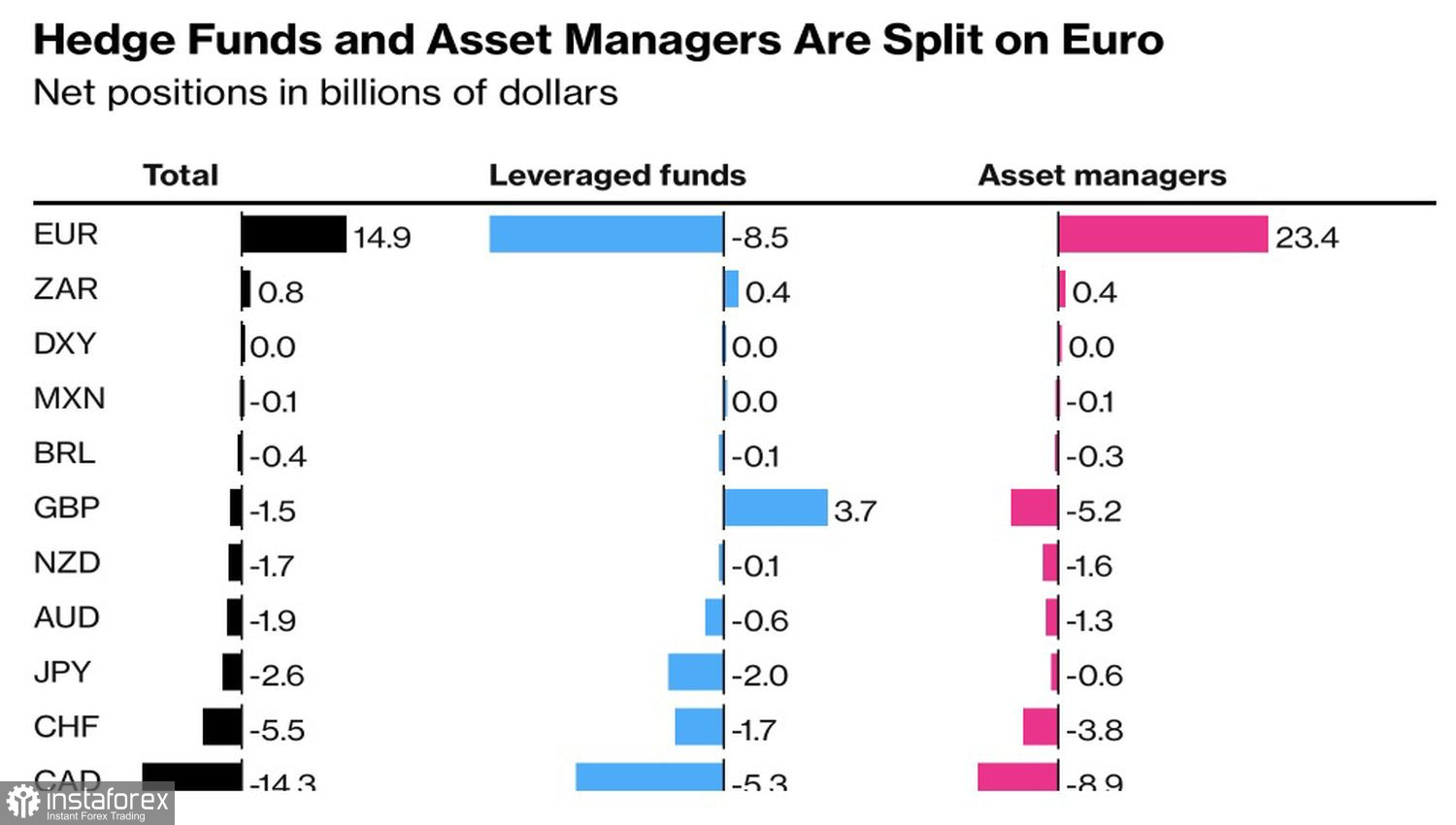

It's no surprise, asset managers are betting heavily on the euro and offloading the regional currency. Their net longs have shrunk from $64 billion in May 2023 to $23.4 billion. Meanwhile, more flexible hedge funds, known for frequently changing positions, have shorted EUR/USD for quite some time.

Bloomberg experts predict the ECB will cut the deposit rate at every meeting until June and then pause it. Borrowing costs are expected to end in 2025 at 2%. Citi disagrees, arguing that the economic impact of trade tariffs on the eurozone will only become apparent in Q3 2024 or later, meaning no pause will occur. Instead, the monetary easing cycle will continue through year-end, with rates falling to 1.5%, below the 1.75% forecasted by the futures market.

Anyone doubting that EUR/USD lacks bearish drivers to continue its southward trajectory is mistaken. The ECB's accelerated monetary expansion and the visibly weakening eurozone economy provide ample motivation for selling the euro.

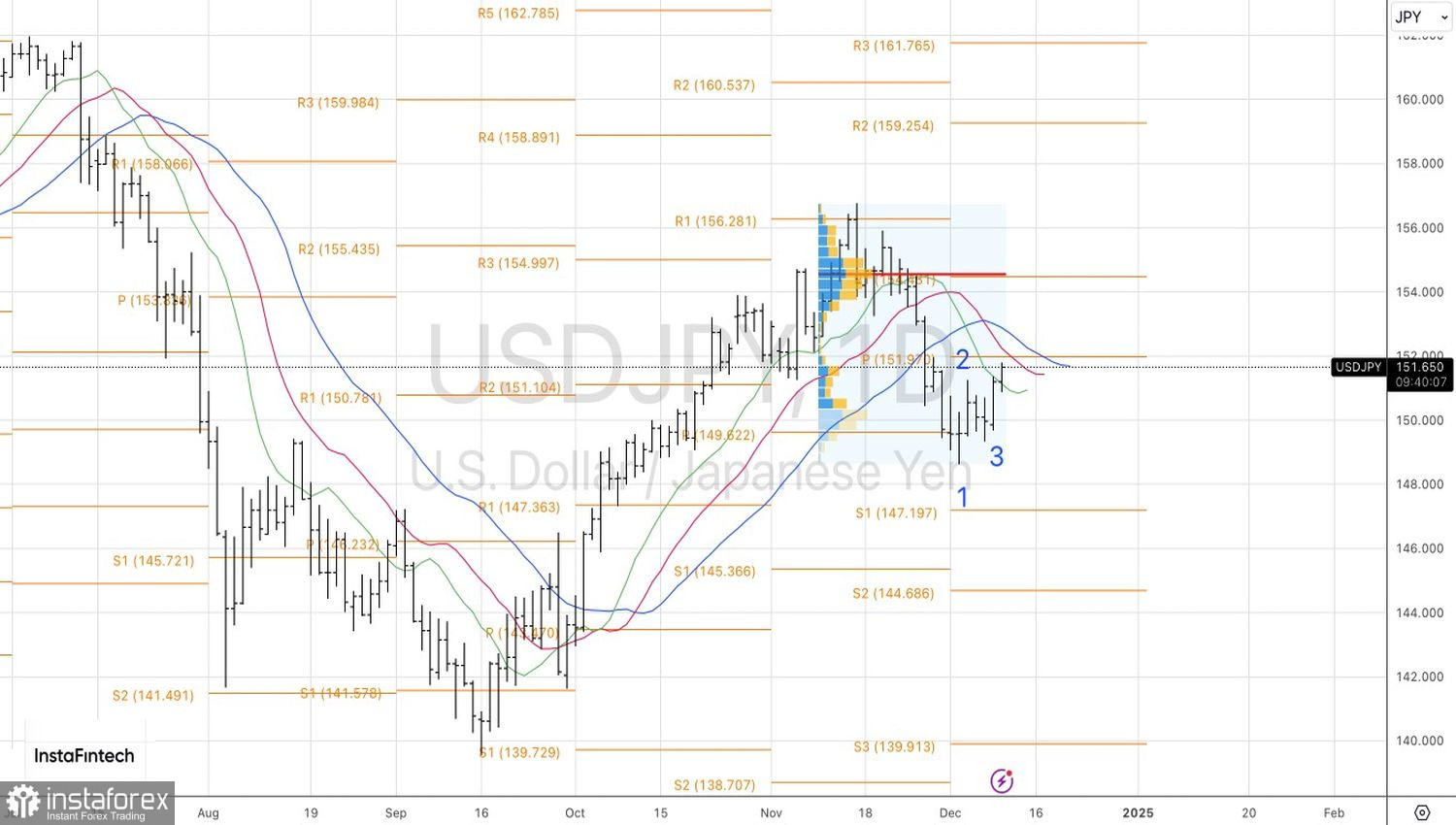

Technically, the daily chart shows that the EUR/USD is resuming its downtrend. The key question is whether support near 1.0465-1.0480 will halt the bears. If it does, the risk of forming and activating a reversal pattern, the Broadening Wedge, will increase. For now, we stick to our selling strategy. Short positions initiated from 1.0550 are being held and periodically expanded.

*El análisis de mercado publicado aquí tiene la finalidad de incrementar su conocimiento, más no darle instrucciones para realizar una operación.

¡Los informes analíticos de InstaSpot lo mantendrá bien informado de las tendencias del mercado! Al ser un cliente de InstaSpot, se le proporciona una gran cantidad de servicios gratuitos para una operación eficiente.