¡La leyenda en el equipo de InstaSpot!

¡Leyenda! ¿Cree que es una retórica grandilocuente? Pero, ¿cómo deberíamos llamar a un hombre, que se convirtió en el primer asiático en ganar el campeonato mundial de ajedrez júnior a los 18 años y en el primer Gran Maestro indio a los 19 años? Ese fue el comienzo de un camino difícil hacia el título de Campeón del Mundo para Viswanathan Anand, el hombre que se convirtió en parte de la historia del ajedrez para siempre. ¡Ahora una leyenda más en el equipo de InstaSpot!

Borussia es uno de los clubes de fútbol con más títulos en Alemania, que ha demostrado repetidamente a los fanáticos: el espíritu de competencia y liderazgo que ciertamente conducirán al éxito. Opere de la misma manera que los profesionales del deporte: con confianza y de forma activa. ¡Mantenga un "pase" del Borussia FC y lidere con InstaSpot!

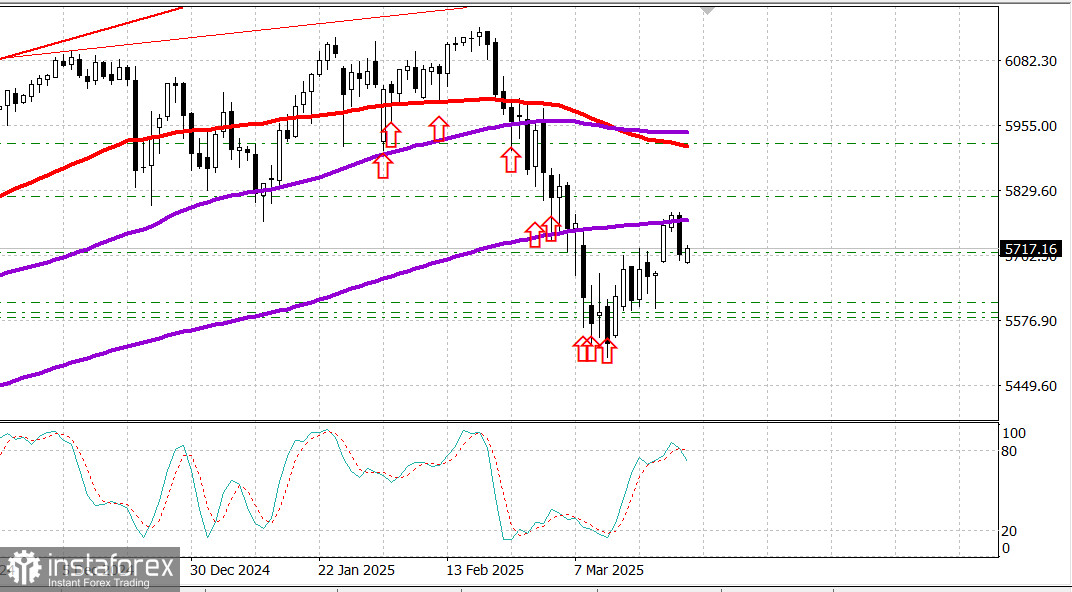

S&P 500

Overview for March 27

The US market dipped on renewed tariff fears and economic uncertainty.

Key US indices on Wednesday: Dow: -0.3%, NASDAQ: -2.0%, S&P 500: -1.1%, S&P 500: 5,712, trading range: 5,500–6,000.

The stock market ended the session in the red across major indices.

The Dow Jones Industrial Average slipped by 0.3%, the S&P 500 lost 1.1%, and the Nasdaq Composite tumbled by 2.0%.

Today's price action pushed the S&P 500 back below its 200-day moving average (5,756), and the Dow, which had turned positive for the year just a day earlier, returned to negative territory for 2025.

There were signs of early buying interest, but mounting losses in mega-cap stocks kept downward pressure on the indices.

Selling intensified in both that segment and across the broader market following reports that President Trump would announce 25% tariffs on imported automobiles. The move is expected to significantly impact car prices and hit key US partners, including Canada, Mexico, and Europe.

Tesla (TSLA 272.06, -16.08, -5.6%) led the decline, pulling back after a strong rebound from a weak start to 2025. Tesla shares remain up 9.4% on the week but are down 32.6% year-to-date.

NVIDIA (NVDA 113.76, -6.93, -5.7%) and other chipmakers also posted steep losses. Reports emerged that the US placed more than 50 Chinese companies on its export blacklist for advanced chips, while the FT reported that new Chinese regulations could hit NVIDIA's sales in the region.

The PHLX Semiconductor Index (SOX) closed down 3.3%. The wave of selling weighed heavily on the S&P 500 information technology sector, which ended as the worst performer of the session by a wide margin.

Next in line for losses were communication services (-2.0%) and consumer discretionary (-1.7%).

On the upside, consumer staples (+1.4%) and utilities (+0.7%), considered defensive sectors, saw the largest gains, reflecting the risk-off tone of the day.

Elsewhere, the Treasury market closed with moderate losses. The 10-year yield rose by 3 basis points to 4.34%, while the 2-year yield edged up by 1 basis point to 4.01%. In this context, today's $70 billion auction of 5-year notes drew weaker demand than yesterday's 2-year offering, but the market reaction remained muted.

Year-to-date performance: Dow Jones Industrial Average: -0.2%, S&P 500: -2.9%, S&P Midcap 400: -4.2%, Nasdaq Composite: -7.3%, Russell 2000: -7.0%

Economic data overview: MBA Weekly Mortgage Applications Index: -2.0% (previous: -6.2%)Durable Goods Orders for February: +0.9% (consensus: -1.2%); Previous reading revised from +3.1% to +3.3% Durable Goods Orders Ex Transportation: +0.7% (consensus: +0.1%); Previous reading revised from 0.0% to +0.1%

The key takeaway from the report is that durable goods orders came in stronger than expected. However, the upbeat headline was offset by a decline in business spending, as evidenced by a 0.3% drop in nondefense capital goods orders excluding aircraft.

Looking ahead to Thursday, market participants will receive the following data:

8:30 AM ET:

Q4 GDP (third estimate; consensus: 2.3%, prior: 2.3%)

Q4 GDP deflator (third estimate; consensus: 2.4%, prior: 2.4%)

Weekly Initial Jobless Claims (consensus: 225,000; prior: 223,000)

Continuing Jobless Claims (prior: 1.892 million)

Advance Goods Trade Balance for February (prior: -$153.3 billion)

Preliminary Retail Inventories for February (prior: -0.1%)

Preliminary Wholesale Inventories for February (prior: +0.7%)

10:00 AM ET:

Pending Home Sales for February (consensus: +2.9%; prior: -4.6%)

10:30 AM ET:

Weekly Natural Gas Inventories (prior: +9 billion cubic feet)

Energy market: Brent crude: $73.70 — Oil is holding at a one-month high despite signs of weakness in the US economy.

Conclusion: Despite yesterday's significant pullback, the bullish trend in the US market remains intact. It is recommended to hold long positions on dips. If you are not yet in the S&P 500, you can buy the SPX instrument at current levels.

*El análisis de mercado publicado aquí tiene la finalidad de incrementar su conocimiento, más no darle instrucciones para realizar una operación.

¡Los informes analíticos de InstaSpot lo mantendrá bien informado de las tendencias del mercado! Al ser un cliente de InstaSpot, se le proporciona una gran cantidad de servicios gratuitos para una operación eficiente.